MARKETTECHGURU — Sunday 24 May 2026

Global Markets Weekly Edition

LIVE DATA — 24 MAY 2026 (Yahoo Finance real-time)

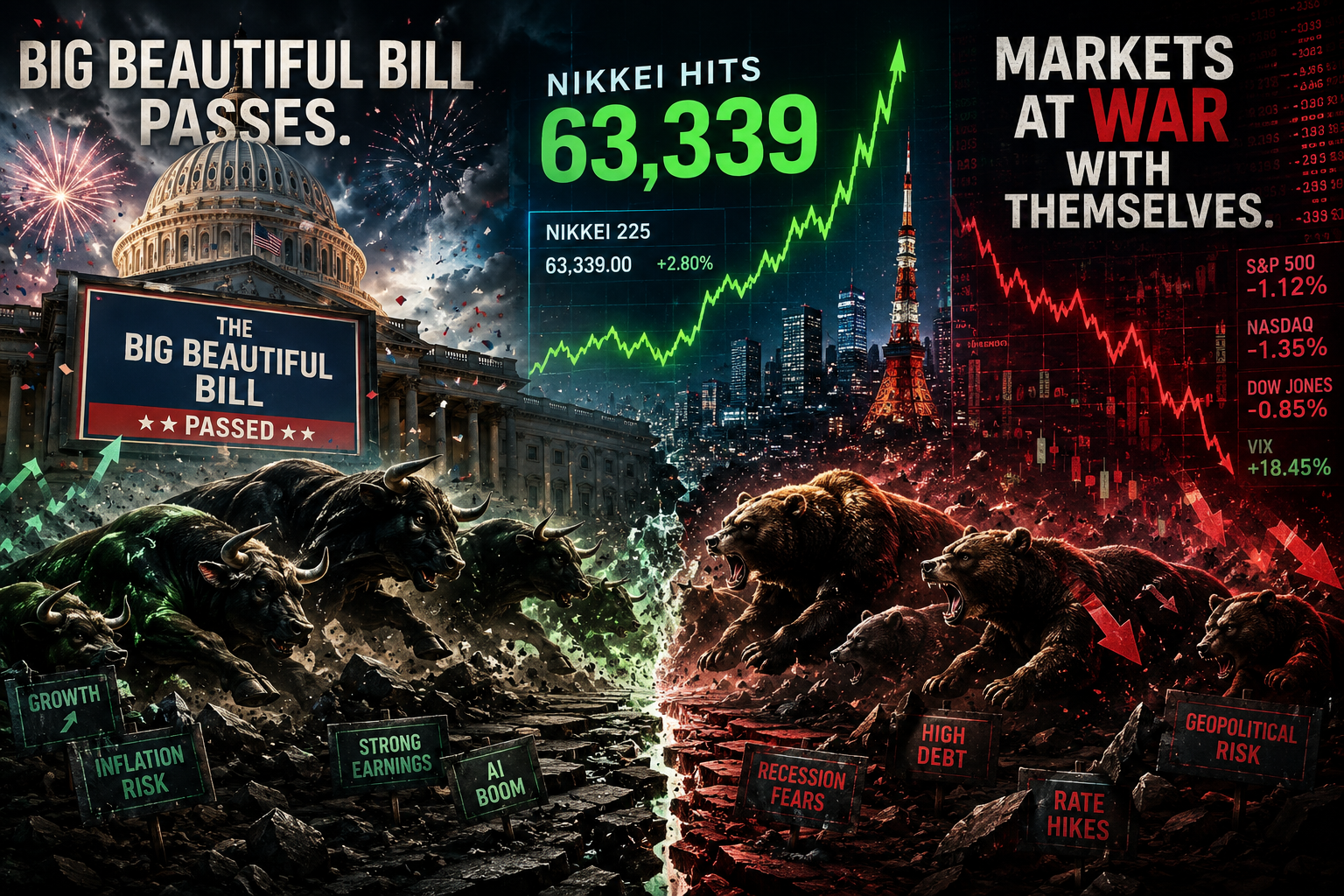

- Nikkei 225: 63,339 (+2.68%) — BEST GLOBAL MAJOR INDEX 🏆

- Dow Jones: 50,579 (+0.58% Friday) — above 50K milestone

- S&P 500: 7,405 (-0.37% live Sunday session)

- Nasdaq: 26,146 (-0.47%)

- DAX Germany: 24,888 (+1.15%)

- FTSE 100: 10,466 (+0.22%)

- CAC 40: 8,115 (+0.37%)

- Euro STOXX 50: 6,019 (+0.99%)

- Hang Seng: 25,606 (+0.86%)

- Shanghai SSE: 4,112 (+0.87%)

- VIX: 16.70 (-0.36%)

- Brent crude: $106.82 (+1.71%)

- Gold: $4,519 (-0.36%)

- Bitcoin: $77,143 (-0.14%)

THE 3 BIG STORIES THIS WEEK

- “ONE BIG BEAUTIFUL BILL” PASSES THE US HOUSE

The most significant fiscal legislation in a generation:

→ Raises US debt ceiling by $5T (largest single increase in US history)

→ Makes 2017 Trump tax cuts permanent

→ No tax on tips, no tax on overtime

→ $150B more defence + $150B more border enforcement

→ CBO projects +$3.8T deficit addition over 2026-2034

→ US 30Y yields spiked on fiscal math concerns

→ Moody’s Aa1 + OBBB = structurally dollar-weakening

UBS: “Persistent deficits and higher Treasury supply could put upward pressure on yields at the long end of the curve.” - WALMART Q1 FY27 BEATS

→ eCommerce: +26% globally

→ US comp sales: +4.1%

→ Operating income: +5% (despite +250bps fuel cost headwind)

→ FY27 guidance maintained: net sales +3.5-4.5%

Signal: US consumer is resilient despite oil shock. Walmart is managing costs. - NIKKEI 63,339 — JAPAN LEADS THE WORLD

+2.68% today. +22%+ YTD. World’s best major index.

AI semiconductors + weak yen + corporate reform + April exports 14.8%.

Still the most underreported winner of 2026.

TODAY’S 6 INVESTMENT OPPORTUNITIES

- GOLD ($4,519) — OBBB STRUCTURAL BULL

US debt + a $5T ceiling raise + Moody’s Aa1 + structural dollar weakness = gold’s medium-term case just got stronger. A dip to $4,519 is tactical. Morgan Stanley year-end target: $5,200. - JAPAN — NIKKEI 63,339

World’s best index. AI supply chain + yen + corporate reform. Target 65K-68K by Q3. - EM AI SUPPLY CHAIN (TSMC, SK HYNIX, PCBs)

Nvidia: $44.1B revenue. TSMC = 12%+ MSCI EM. OBBB fiscal boost → US tech capex → EM manufacturers benefit. Structural multi-year supercycle. - INDIA SENSEX — ASYMMETRIC IRAN DEAL TRADE

-11.6% YTD. 85% oil importer. The Iran deal is still in its “final stage.” Hormuz confirmation = a +5-8% single-session rally. The most asymmetric EM trade alive. - SHORT-US LONG-DURATION

30Y yields at Oct-2023 highs. OBBB adds $3.8T. Yale: 10Y yield is +1.2 pp from bill alone. Avoid TLT. Rotate to EM local bonds at 9%+. - BITCOIN ($77,143) — FISCAL DEBASEMENT PLAY

$5T debt ceiling raise = dollar debasement narrative. Every major US fiscal expansion preceded a BTC rally. Analyst targets $100K-$150K for 2026 cycle.

Sources: Yahoo Finance · Walmart SEC · UBS · FX Street · Crestwood Advisors · Trading Economics · CBO. Not investment advice.