The headlines say prices are up. Developers are celebrating record launches. Property portals are running full-page ads about a booming market. And somewhere in the fine print — buried in RERA filings that nobody reads — is a completely different story.

“The Indian real estate market is the most headline-managed asset class in the country. I dug into the RERA filings so you don’t have to. What I found should change how every buyer and investor thinks about property.”

Before we look at the data, let’s establish the most important thing you need to understand about Indian property prices: the price you read in headlines is almost never the price paid in reality.

The Three Gaps Nobody Talks About

Gap 1: Asking price vs. transaction price. Every major property portal — Magicbricks, 99acres, Housing.com — reports listing prices set by developers and brokers. These are asking prices. The actual registered sale price (filed with the sub-registrar) can be 10–25% lower, particularly in premium segments and slow-moving micro-markets. You are reading marketing, not data.

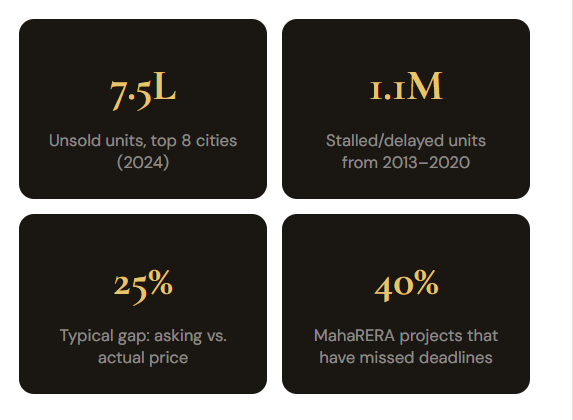

Gap 2: Launches vs. completions. The industry celebrates project launches as demand signals. But India has one of the worst housing completion records in the world. Over 1.1 million apartments launched between 2013 and 2020 remain incomplete—buyers are stuck paying EMIs on homes that don’t exist yet. A launch announcement is not a sale, and a sale is not a home.

Gap 3: Inventory vs. absorption. India’s unsold inventory stood at approximately 7.5 lakh units across its top 8 cities as of 2024. At current absorption rates, that’s 3–4 years of supply sitting in the market. A market with four years of unsold inventory is not booming. It is carefully managed to appear that way.

Reading the RERA Data: What It Actually Says

RERA was supposed to fix all of this. Introduced in 2016, it mandated developer registration, quarterly progress reports, and escrow accounts for 70% of buyer funds. And it has helped—but the data it generates tells a story the industry desperately wants to ignore.

In Maharashtra, approximately 40% of RERA-registered projects have missed their declared completion date at least once. In Karnataka, the figure is closer to 45%. MahaRERA alone had received over 40,000 complaints by 2024 — and these are only the buyers who bothered to file. The actual grievance rate is far higher.

The most cynical development: after COVID, developers across every state applied for and received 1–2-year extensions by citing pandemic disruption. Many of these projects already had pre-COVID delays. The pandemic became a blanket excuse to push already-delayed timelines further—with regulatory blessing.

The City-by-City Picture

🔴 NCR — Extreme Caution

150,000+ stalled units from 2010–2016. Jaypee, Amrapali, and others left buyers in legal limbo for a decade. New launches sell, but the legacy baggage is enormous.

🟡 Mumbai MMR — Expensive But Real

Most liquid market in India. Constrained by geography. Price-to-income ratio now 14–15x. Affordable housing is effectively dead in Mumbai proper.

🟢 Hyderabad — Closest to Rational

Genuine IT employment-driven demand. ₹5,000–8,000/sq ft in the Western corridor. Lower inventory overhang. Better builder completion record than peers.

🟡 Bengaluru — IT-Dependent

Split market: Whitefield and Marathahalli have genuine end-user demand; North Bengaluru is speculative. Tightly linked to IT hiring cycles.

What Buyers Must Do Right Now

If you are in the market to buy, here is the non-negotiable checklist — things your property broker will never volunteer because their commission depends on you signing quickly:

- Check the RERA portal for your state. Free. Takes 5 minutes. Search the project, check the declared completion date, look for revised timelines, and count the complaints filed. A developer with 50+ complaints is a different proposition from one with 5.

- Apply the 30% rule without exceptions. Total EMIs across all loans should never exceed 30% of take-home salary. If buying pushes you above this, you are buying too much house. Wait or buy smaller.

- Buy ready-to-move only, for now. The under-construction discount does not compensate for the delay risk in the current market. Pay the premium for certainty — your time and peace of mind are worth more.

- Spend ₹20,000 on proper title verification.60% of Indian property disputes trace back to title defects that due diligence would have caught. A property lawyer checking 30 years of title chain is the best insurance you’ll ever buy.

- Negotiate. Everyone does — nobody admits it.Developers are sitting on inventory. Most will negotiate 5–15% on base price or offer equivalent value in free parking, club memberships, or fitments. The asking price is a starting point.

- Compare honestly with REITs.India’s listed REITs — Embassy, Mindspace, Brookfield, Nexus — offer 6–7% rental yields with full liquidity and zero management headaches. If your goal is investment returns, run this comparison before signing anything.

The Investment Verdict

Indian real estate is not crashing. But it is also not the one-way escalator that developer advertising implies. The honest picture is more complex: a market with pockets of genuine demand surrounded by a sea of inherited excess supply, managed narrative, and regulatory loopholes that still haven’t fully closed.

The buyers who will do well are the ones who ignore the headlines, read the RERA data, buy what they can actually afford, and choose cities and micro-markets where real jobs are being created. That’s Hyderabad’s Western corridor, Bengaluru’s Whitefield, Pune’s Hinjewadi, and Chennai’s OMR. Not speculative suburban launches 40 kilometers from the nearest employment hub.

Property is still a valid asset class in India. But only if you approach it like an investor — not like someone who just watched a developer’s YouTube ad.

Get The Big Picture — every day on LinkedIn.

Deep analysis on markets, property, and the economy. No noise, no sponsored takes. Subscribe free.

Subscribe →