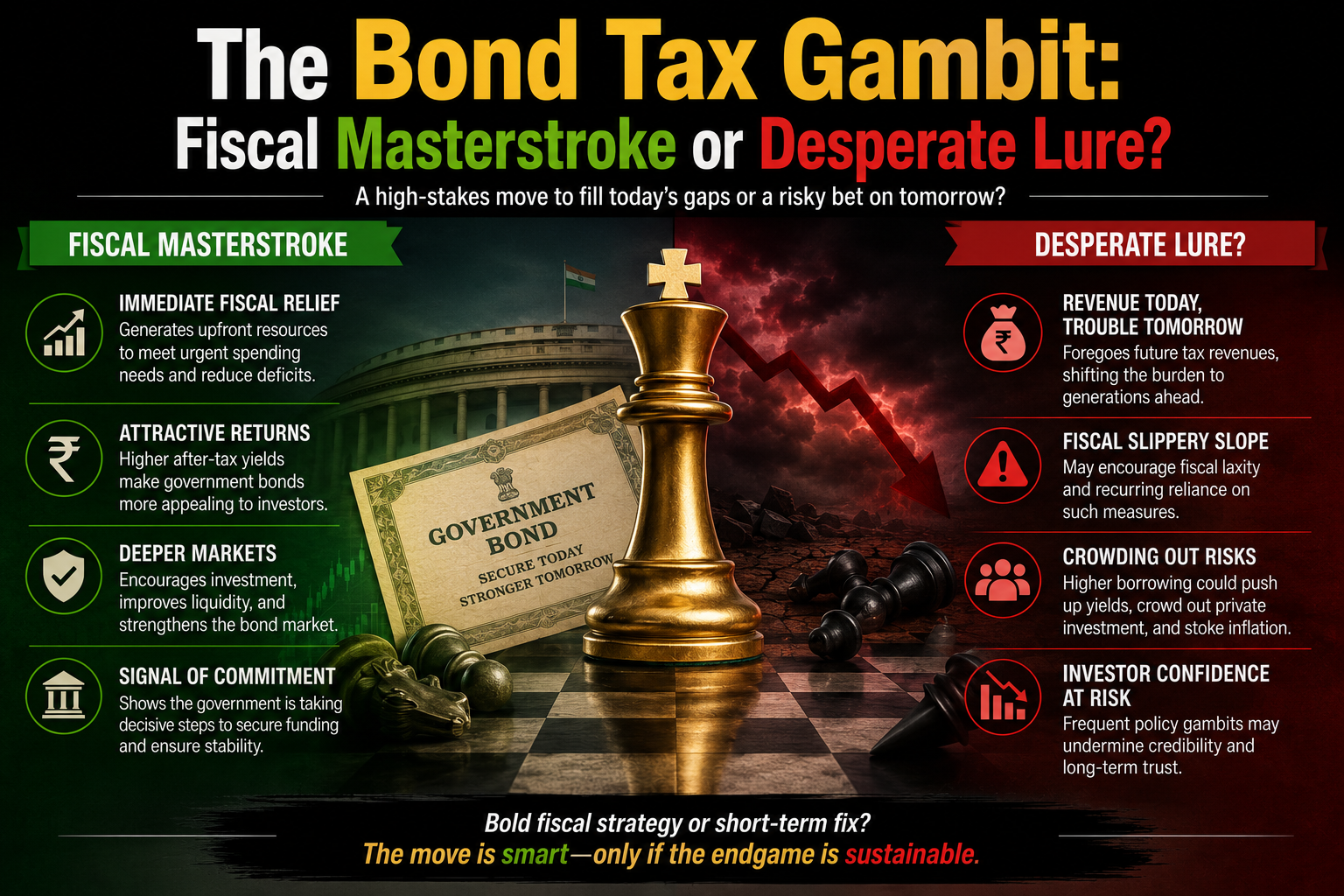

Reports suggest the Indian government is weighing a reduction in withholding tax on

bond investments by foreign investors. On the surface, it’s a move to sweeten the pot

for FPIs (Foreign Portfolio Investors) following India’s inclusion in global bond indices.

But is it the right move for the Indian economy at large?

- The “Index Inclusion” Paradox

India’s entry into global bond indices (like JP Morgan’s) was supposed to bring in

billions of dollars automatically. If the “inclusion” is already doing the heavy lifting,

Why the rush to slash taxes now? This move signals a slight anxiety that the expected

inflows might not be as aggressive as projected, or perhaps, the government is trying

to offset the recent volatility in global yields.

- Revenue Leakage vs. Liquidity Gain

A lower withholding tax means less revenue for the national exchequer. In an era

where fiscal consolidation is the mantra, giving a tax break to foreign capital—while

domestic investors continue to pay standard rates—creates a tiered playing field. We

must ask: Inflow × Velocity > Tax Revenue Loss? If the liquidity doesn’t translate into

Lower borrowing costs for Indian corporates are a net loss for the taxpayer. - The Rupee Risk

Inviting “Hot Money” through tax incentives is a double-edged sword. While it

supports the Rupee in the short term, it makes the currency more vulnerable to

global “risk-off” sentiments. When the Fed moves, these tax-incentivized investors

are often the first to pull the trigger, leading to sharper currency depreciation.

“Lowering taxes for foreigners might stabilize the bond market today, but it

potentially increases the cost of currency defense tomorrow.”

Summary

The proposed tax cut is a classic liquidity play. It aims to make Indian debt irresistible

to global funds. However, the government must ensure that this “red carpet”

Treatment doesn’t come at the cost of domestic financial stability or fiscal prudence.