Introduction

Here’s a number that should reframe how you think about 2026: emerging market stocks have outperformed the S&P 500 for five straight quarters, and they’re on track for a sixth. Not because Wall Street stumbled — the S&P 500 is still posting solid gains — but because the AI trade has found a second engine, and that engine is built in Taiwan, assembled in South Korea, and increasingly financed in Mumbai.

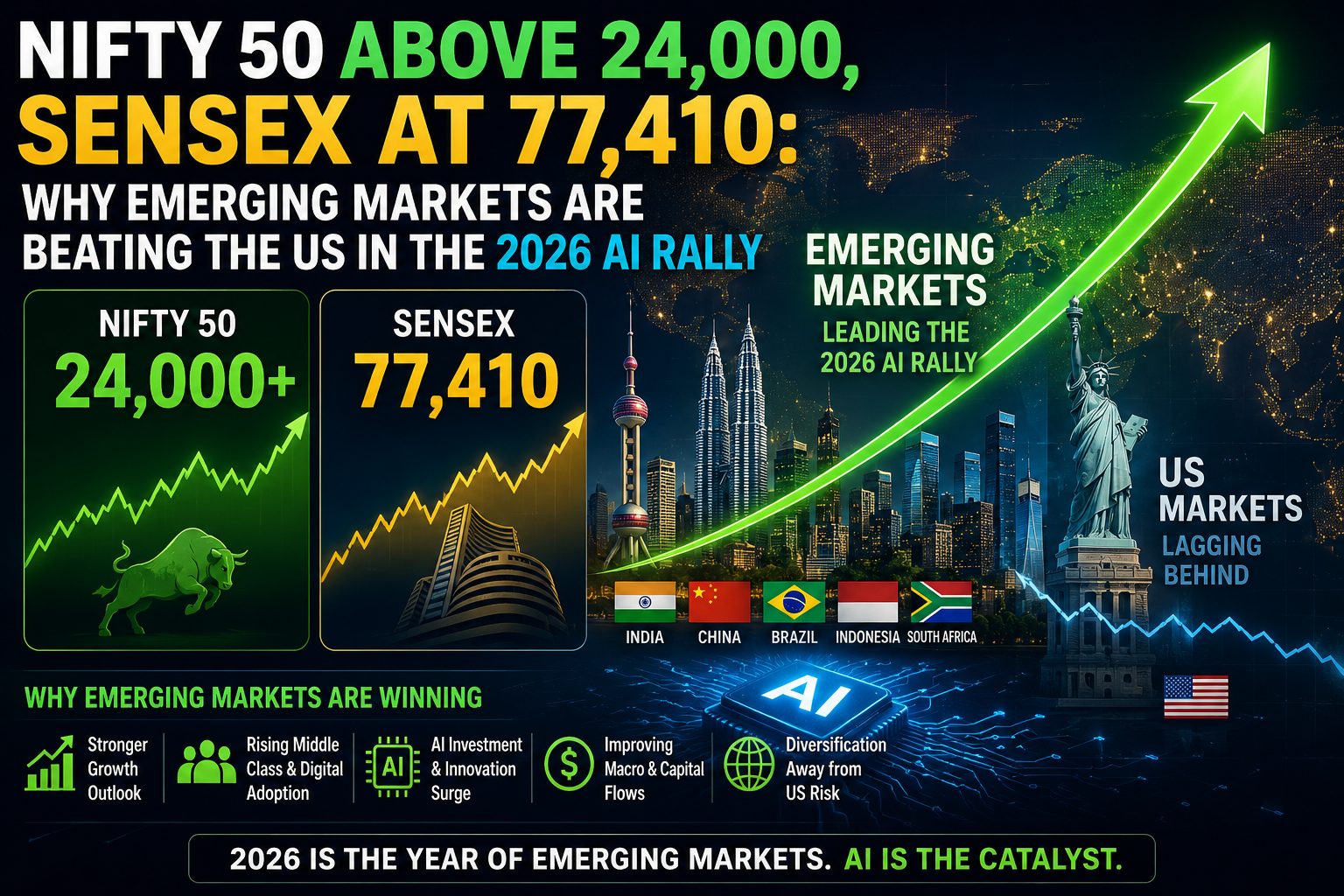

On June 18, 2026, the BSE Sensex closed at 77,410, its fifth consecutive session of gains. The Nifty 50 is trading comfortably above the 24,000 mark. These are headline-grabbing numbers for Indian investors who have weathered a choppy 12 months. But here’s the part most domestic coverage is missing: India’s rally is the junior partner in a much larger emerging-markets story — one where Taiwan and South Korea, not India, have captured the lion’s share of AI-driven capital. Understanding why matters enormously for how you position a portfolio in the second half of 2026.

This isn’t a simple “EM is back” story. It’s a story about who actually owns the AI supply chain, why the dollar’s trajectory matters more than most retail investors realize, and why India’s market resilience in 2026 has come from an unlikely source—not foreign money, but the disciplined, almost stubborn buying power of Indian retail investors through SIPs.

What Is Happening?

Global capital is rotating. For most of the last decade, “AI trade” was shorthand for US mega-cap tech—the Magnificent Seven, Nvidia, and the Nasdaq. That hasn’t reversed, but it has been joined by a parallel rally in emerging markets, and in 2026 the EM leg has actually outrun the US leg.

The numbers tell the story plainly. The MSCI Emerging Markets Index has climbed sharply since the start of 2026, decisively outperforming the S&P 500’s more modest single-digit gain over the same stretch. Within that EM basket, the gains are extraordinarily concentrated: South Korea’s KOSPI has rallied roughly 87% year-to-date, and Taiwan’s market has surged more than 50%, both powered by semiconductor earnings tied directly to AI infrastructure buildout. Taiwan’s stock market has even overtaken India’s to become the world’s fifth largest, trailing only the US, mainland China, Japan, and Hong Kong.

Meanwhile, India has been doing something different — and arguably more interesting. The Sensex’s climb to 77,410 wasn’t primarily a foreign-money story. Through much of 2026, foreign portfolio investors (FPIs) were net sellers of Indian equities, pulling out an estimated ₹2.2 lakh crore (roughly $30 billion) by early June — even as some of that same capital flowed into South Korea and Taiwan instead. What kept Indian markets afloat was domestic money: mutual fund SIP contributions and institutional buying that absorbed nearly all of the foreign selling.

Why It Matters

This matters on three levels.

First, it changes the diversification calculus. For years, “international diversification” meant adding a thin sliver of EM exposure as a hedge, expecting it to lag the US in good times and crater faster in bad times. That correlation has weakened. EM equities are now compounding AI-driven earnings growth that, in some pockets, exceeds what’s priced into US tech. A portfolio with zero EM exposure in 2026 has structurally underweighted the most productive part of the global AI trade.

Second, it exposes how concentrated the “EM AI trade” really is. This is not a broad-based emerging markets renaissance. It is, in large part, three companies—Taiwan Semiconductor Manufacturing Co. (TSMC), Samsung Electronics, and SK Hynix—which together account for close to 30% of the MSCI EM Index. Taiwan and Korea combined make up roughly half the index. If you bought a generic “emerging markets” fund this year, you bought a leveraged bet on the AI hardware supply chain whether you realized it or not.

Third, it reveals something important about India specifically. India’s market strength in 2026 has come despite being underweighted in the AI hardware rotation, not because of it. That’s a structurally different — and arguably more durable — story than Taiwan’s or Korea’s, because it isn’t dependent on semiconductor cycle timing. But it also means Indian investors shouldn’t assume the Sensex’s rise reflects the same AI tailwind lifting Seoul and Taipei. It largely doesn’t.

Key Drivers

1. AI capital expenditure cascading into hardware earnings. Hundreds of billions of dollars in global AI data center spending flow disproportionately to a small number of chip and memory manufacturers. TSMC dominates advanced chip fabrication; SK Hynix and Samsung lead high-bandwidth memory production essential for AI servers. Analysts expect another year of outsized earnings growth in the region’s technology hardware and semiconductor sectors.

2. A structurally softer US dollar. A weakening greenback has historically been one of the strongest tailwinds for emerging-market equities, lowering the cost of dollar-denominated debt for EM economies and making EM assets more attractive on a relative-return basis. The dollar index has been testing long-term technical support, and further weakness would extend this EM tailwind.

3. Valuation gap. Despite the rally, MSCI’s emerging index trades at a roughly 44% discount to the S&P 500 on forward earnings multiples—the widest gap in over a year. That discount has narrowed less than earnings have grown, meaning much of the EM re-rating has come from upgraded profit forecasts (EM companies have seen profit estimates lifted roughly 30% this year, versus around 10% for the S&P 500) rather than speculative multiple expansion.

4. India’s domestic liquidity machine. RBI rate cuts — a cumulative 100+ basis points of easing through the December 2025 policy cycle, bringing the repo rate to 5.25% — have lowered borrowing costs and supported rate-sensitive sectors like banking, auto, and real estate. Indian equity mutual funds have now logged over five consecutive years of positive monthly inflows, with SIP contributions remaining remarkably stable even during market stress.

5. Easing geopolitical risk. A US-Iran interim ceasefire agreement helped pull crude oil prices lower in mid-June, directly benefiting import-dependent economies like India by easing inflation and current account pressure — a key factor behind the Sensex’s five-session winning streak into the 77,410 close.

Winners and Losers

Likely winners:

- Taiwanese and Korean semiconductor and memory manufacturers—TSMC, Samsung Electronics, and SK Hynix—remain the most direct beneficiaries of AI infrastructure spending.

- Indian public-sector and private banks—lower rates and strong domestic credit growth have made financials one of India’s best-performing sectors in 2026, with State Bank of India alone carrying over 51% weight in the banking index’s rally.

- Indian auto and real estate—both sectors posted sharp gains immediately following the RBI’s rate cut, as lower EMIs improve affordability.

- Indian defense and capital goods—names like Bharat Electronics have featured among recent top Sensex gainers amid sustained government capex.

- EM-focused active ETF managers—a wave of newly launched, actively managed EM ETFs are emerging specifically to help investors access AI supply-chain exposure while diversifying beyond the three mega-cap chip names.

Likely losers (or at-risk):

- Indian IT services exporters—Infosys, TCS, Tech Mahindra, and HCL Tech—were among the worst performers in the Sensex’s recent sessions, pressured by expectations of higher US interest rates and softer demand commentary from global peers like Accenture.

- EM countries without an AI/tech angle—markets without semiconductor, hardware, or AI-adjacent exposure risk being left out of the rotation entirely, even within the “emerging markets” label.

- Passive EM index investors who don’t understand concentration risk — a market-cap-weighted EM fund is now, in effect, a concentrated bet on three chip companies; investors expecting broad diversification may be surprised by the correlation to semiconductor cycles.

- Currency-sensitive importers — if EM strength reverses alongside a dollar rebound, countries running large import bills (India included, given oil dependence) would feel it quickly through currency depreciation.

Indian Perspective

India’s 2026 story is genuinely distinct from the Taiwan/Korea AI hardware narrative, and that distinction is the most important nuance for domestic investors to internalize.

While Taiwan and Korea have captured AI capex flows directly through chip manufacturing, India has captured almost none of that hardware upside—Indian semiconductor manufacturing remains nascent despite government incentive schemes. Instead, India’s rally has been built on three different pillars: domestic monetary easing, resilient consumption and credit growth, and the structural shift of Indian equity ownership toward domestic hands.

That last point deserves emphasis. FPI ownership of Indian listed stocks has fallen to roughly 14.7% — a 14-year low — while domestic institutional investors now hold a larger share of the market than foreign investors for what may be the first time in over a decade. Some of the very capital that exited India in 2026 was redirected into Taiwan and South Korea, chasing the AI hardware trade more directly. In April alone, FIIs sold over $1 billion in Indian equities while allocating roughly $1 billion to South Korea and $1.5 billion to Taiwan — a clear, quantifiable rotation.

What absorbed that selling? Domestic mutual funds, insurance companies, and pension funds, fueled by SIP inflows that crossed ₹4.3 trillion in the first half of 2026 alone, covered nearly all of the FPI outflow. This is arguably the more important Indian market story of 2026: a maturing, self-sustaining domestic capital base that no longer panics when foreign money exits.

Sectors and opportunities for Indian investors:

- Banking and financial services — direct beneficiaries of rate cuts, credit growth, and digital lending expansion.

- Consumption-linked sectors (auto, FMCG, real estate) — supported by the GST 2.0 rate rationalization (28% to 18% on select goods) and income tax relief raising effective tax-free income to ₹12 lakh, both of which boost disposable income.

- Defense and capital goods—sustained by government infrastructure and defense capex.

- Selective IT exposure to weakness—the sector’s underperformance may present value for long-term investors if US enterprise AI spending eventually flows through to Indian IT services demand, though near-term headwinds remain real.

- India’s own semiconductor ambitions — still early-stage, but a multi-year theme worth monitoring as government incentives mature.

Global Perspective

Globally, 2026 is shaping up as the year the “Magnificent Seven vs. the rest” framework broke down. The broader story is that the rest of the world’s stock markets, measured collectively, have outperformed US markets over the trailing year for the first time since the early 2000s — a reversal that strategists at major firms have flagged as a meaningful structural shift, not a one-quarter blip.

Geographic diversification within EM itself has also been notable. Earlier rotations favored China and South Africa; more recently the baton has passed decisively to North Asia’s chip exporters. South African equities, for context, rose roughly 60% in a prior period on fiscal consolidation and a sovereign credit upgrade—a reminder that EM outperformance isn’t monolithic and different economies are winning for different reasons at different times.

The bigger global question is durability. Periods of EM outperformance versus the US have historically run in long, multi-year cycles—the 2003–2010 stretch being the most cited precedent. If 2026 marks the start of a similar cycle, the valuation gap between EM and US equities still has room to close.

Investment Opportunities

For investors looking to act on this trend without naive concentration risk, consider:

- Broad MSCI EM index funds or ETFs, understanding that you are implicitly taking concentrated semiconductor exposure through Taiwan and Korea.

- Actively managed EM funds that explicitly diversify beyond the three largest chip names into the broader AI supply chain—smaller-cap semiconductor suppliers, AI infrastructure beneficiaries, and deglobalization/reshoring plays.

- India-focused funds tilted toward domestic consumption and financials, rather than IT services, to align with India’s actual 2026 growth drivers rather than the AI hardware narrative.

- Currency-hedged EM exposure for investors concerned about dollar reversal risk.

- Indian government and corporate bonds, which have benefited from India’s continued inclusion in global bond indices (JP Morgan GBI-EM, Bloomberg EM Local Currency Index), offering a different risk profile than equities.

Risks Investors Should Watch

- Semiconductor cycle reversal. The EM rally’s heaviest weight rests on AI capex continuing at its current pace. Any slowdown in hyperscaler spending or order volumes would hit Taiwan and Korea disproportionately hard, and by extension, the entire MSCI EM Index.

- Dollar rebound. A reversal in dollar weakness — for instance, from renewed Fed hawkishness — would remove one of EM’s biggest 2026 tailwinds. Notably, the Fed has already signaled it kept rates unchanged while leaving the door open to a hike later this year, a meaningfully hawkish tone that markets are still digesting.

- Geopolitical fragility. The US-Iran ceasefire that helped lower oil prices and support Indian markets remains “interim,” not permanent. Renewed conflict would reverse the oil-price tailwind quickly.

- India-specific FPI disengagement. Continued foreign selling, even if absorbed by domestic flows, signals that global allocators currently prefer direct AI hardware exposure (Taiwan, Korea) over India’s more diversified, consumption-driven growth story. A prolonged preference shift could cap India’s relative re-rating versus peers.

- Concentration risk inside “diversification.” Investors buying EM funds for diversification away from US mega-cap tech concentration may be unknowingly buying a different flavor of the same concentration problem.

What Happens Next?

Watch three things over the second half of 2026: whether AI hyperscaler capex guidance holds up through earnings season, whether the Fed’s hawkish tilt translates into an actual rate hike (which would pressure both US and EM risk assets), and whether Indian FPI flows stabilize or continue rotating toward North Asia. Domestic Indian flows have proven resilient, but they cannot indefinitely offset large, sustained foreign selling without eventually showing strain in valuations or liquidity.

Key Takeaways

- EM equities have outperformed the S&P 500 for five consecutive quarters, driven overwhelmingly by AI-linked semiconductor and memory companies in Taiwan and South Korea.

- India’s 2026 rally to Sensex 77,410 and Nifty above 24,000 is real, but it is a domestic liquidity and rate-cut story, not primarily an AI hardware story.

- Foreign investors have been net sellers of Indian equities in 2026 even as they bought aggressively into Taiwan and Korea — a quantifiable rotation within EM itself.

- Domestic SIP flows and institutional buying have structurally changed Indian market ownership, with domestic investors now holding more of the market than foreign investors for the first time in over a decade.

- EM valuations remain meaningfully cheaper than US equities on a forward earnings basis, even after the rally.

Conclusion

The headline numbers—Nifty above 24,000, Sensex at 77,410, EM beating the US—are accurate, and they matter. But the real story for 2026 is more textured than “emerging markets are back.” It’s a story about a narrow, AI-hardware-driven rally concentrated in Taiwan and Korea, running in parallel to a separate, domestically financed Indian rally built on rate cuts and an increasingly self-reliant retail investor base. Both are legitimate trends. Conflating them risks misreading what’s actually driving your portfolio’s returns — and what could end them.

FAQ Section

1. Why is the Nifty 50 above 24,000 right now? The Nifty’s rise reflects RBI rate cuts that have lowered borrowing costs, easing crude oil prices following a US-Iran ceasefire, and sustained domestic mutual fund buying that has offset persistent foreign portfolio outflows.

2. Is India’s stock market rally connected to the global AI boom? Only indirectly. Unlike Taiwan and South Korea, India has limited semiconductor manufacturing exposure, so its 2026 rally has been driven more by domestic monetary policy and consumption than by AI hardware earnings.

3. Why are foreign investors selling Indian stocks even as the market rises? FPI ownership of Indian equities has fallen to a 14-year low as global allocators have rotated capital toward more direct AI hardware plays in Taiwan and South Korea. Domestic institutional and retail (SIP) buying has absorbed most of this foreign selling.

4. What is the MSCI Emerging Markets Index, and why does it matter? It’s the most widely tracked benchmark for emerging-market equities, used by most global EM ETFs and funds. In 2026, it has been heavily concentrated in Taiwan, South Korea, and a handful of AI-linked semiconductor companies, meaning broad EM exposure now carries significant tech-sector concentration.

5. Should I invest in emerging markets or just stick with the US market? That depends on your risk tolerance, time horizon, and existing portfolio concentration. EM offers a lower valuation entry point and exposure to the AI hardware supply chain but carries currency, geopolitical, and concentration risks the US market doesn’t. Many strategists suggest EM as a complement to, not a replacement for, US equity exposure. This isn’t individual financial advice—consult a licensed advisor for your specific situation.

6. What sectors are driving the Sensex and Nifty rally? Banking, financials, auto, and real estate have led, supported by lower interest rates. IT services have lagged due to concerns about US demand and higher-for-longer US rates.

7. Is the EM rally sustainable, or is it a bubble? Valuations suggest it isn’t purely speculative — EM earnings estimates have been upgraded far more than US estimates this year, and the EM-to-US valuation discount remains historically wide. However, the rally’s heavy concentration in a few chip companies means it’s vulnerable to any AI capex slowdown.

8. How does a weaker US dollar help emerging markets? A weaker dollar reduces the cost of servicing dollar-denominated debt for EM economies, makes EM assets cheaper and more attractive to global investors, and historically correlates with periods of EM outperformance.

9. What is the difference between FII and DII flows in India? FIIs (Foreign Institutional Investors) are overseas funds; DIIs (Domestic Institutional Investors) are Indian mutual funds, insurers, and pension funds. In 2026, sustained DII buying — powered by retail SIP inflows — has offset large FII selling, a structural shift in who actually owns Indian equities.

10. What risks could end the emerging markets rally? A slowdown in global AI infrastructure spending, a reversal in dollar weakness (especially if the Fed turns more hawkish), renewed geopolitical conflict affecting oil prices, or a broader risk-off shift in global markets are the primary risks to watch.

Recommended Reading: 📚 THE LIQUIDITY CYCLE: How Global Money Flows Create Booms, Busts, and Investment Opportunities: An Institutional-Grade Guide to Profiting from Global Liquidity Cycles